Everyone talks about coverage. Very few talk about the part you pay.

And that’s the deductible.

It’s the number that decides whether filing a claim makes sense… how much money actually comes out of your pocket, and why some “approved” claims still feel expensive. Most homeowners think they understand deductibles, until the first real claim.

The Deductible Is Not What Most People Think

Ask a homeowner what a deductible is, and you’ll usually hear a short answer.

“It’s what I pay first.”

That’s not wrong, but it’s incomplete.

A deductible isn’t just a bill you pay before insurance helps. It’s a cost-sharing rule built into the policy. And that rule affects when you file claims, how much you receive, and sometimes whether filing is worth it at all.

The deductible exists for one reason: to separate small, manageable losses from larger ones insurance is designed to handle.

Insurance isn’t meant to pay for every scratch, leak, or minor repair. The deductible creates a buffer, sort of a line you cross before insurance steps in.

But here’s where confusion starts.

Many people assume the deductible is subtracted from the total repair cost. Others think it resets yearly. Some believe insurance sends them a bill for it.

In reality, the deductible is usually withheld from the claim payment, not paid directly to the insurer. You pay it as part of the repair cost, not as a separate transaction.

Understanding that difference matters.

Because once you see how deductibles actually work, you stop asking, “Is this covered?”, and start asking the better question concerning “Is this worth filing a claim for?”

Different Types of Home Insurance Deductibles

Not all deductibles work the same way.

Most homeowners think of a deductible as one fixed dollar amount, but many policies actually include multiple deductible types, depending on the kind of claim.

The most common is a flat-dollar deductible. This is a set amount, like $500, $1,000, or $2,500, that applies to most everyday claims. If repairs cost more than that amount, insurance pays the rest, minus the deductible.

Then there are percentage-based deductibles, which surprise a lot of people the first time they encounter them. Instead of a flat number, the deductible is a percentage of the home’s insured value. A 1% deductible on a $300,000 home means you’re responsible for $3,000 before insurance pays anything. A 2% deductible doubles that.

These percentage deductibles are most commonly tied to wind, hail, or hurricane claims, depending on location.

Some policies also separate deductibles by peril, one amount for general claims, another for specific risks like storms. This matters because homeowners often think they have a low deductible, only to discover that the type of damage they’re dealing with triggers a much higher one.

Understanding which deductible applies and when, is essential. Because the deductible you think you have isn’t always the one that shows up after a loss.

How Deductibles Are Actually Applied To The Claim

One of the most persistent misunderstandings about deductibles is how they’re actually used.

Insurance doesn’t usually send you a bill for your deductible.

Instead, the deductible is subtracted from the claim payment.

If approved repairs total $12,000 and your deductible is $2,000, the insurer typically pays $10,000. You cover the remaining $2,000 directly through repair costs.

This distinction matters because it affects cash flow and expectations.

Another important point: the deductible usually applies once per claim, not per repair. If multiple damages stem from the same covered event, they’re generally grouped under a single deductible.

But separate events mean separate deductibles even if they happen close together.

Timing matters here.

If a storm damages your roof and weeks later a different issue causes interior damage, those may be treated as two separate claims with two separate deductibles. This is also why smaller claims often don’t make financial sense to file.

If the repair cost is close to or below your deductible, insurance won’t meaningfully help. And filing can still impact your claims history.

Once homeowners understand how deductibles are applied, they start evaluating claims differently, not emotionally but strategically.

And that’s exactly how deductibles are meant to shape behavior.

Why A Higher Deductible Often Lowers Your Premium

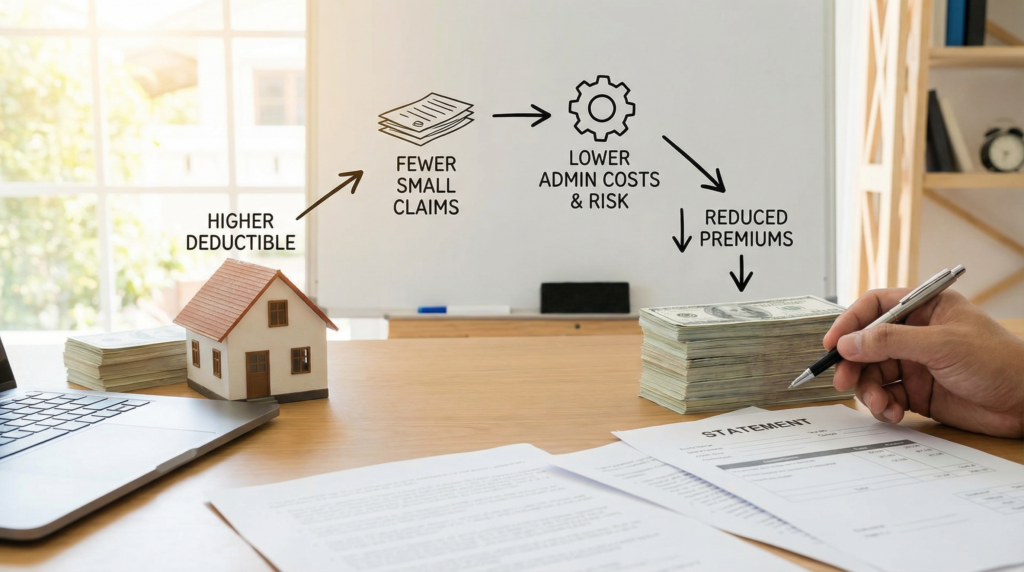

Deductibles don’t just affect claims. They also affect what you pay every month.

When you choose a higher deductible, you’re agreeing to take on more risk yourself. And in exchange, the insurer charges a lower premium.

From the insurance company’s perspective, this makes sense.

Higher deductibles reduce the number of small claims. Fewer small claims mean lower administrative costs and lower overall risk. That savings gets passed back to the homeowner in the form of reduced premiums.

But the trade-off is real. A lower premium feels good every month. A higher deductible hurts all at once and when something actually goes wrong.

This is why deductible choice isn’t about finding the cheapest option. It’s about choosing the level of risk you can comfortably absorb without stress.

If a $3,000 deductible would force you to put repairs on a credit card or delay fixing damage, the premium savings may not be worth it. On the other hand, if you have emergency savings and want to minimize monthly costs, a higher deductible can make sense.

The right deductible is personal. It depends less on the house and more on your financial flexibility.

When Filing a Claim Doesn’t Make Sense

One of the most practical uses of understanding your deductible is knowing when not to file a claim.

If the repair cost is close to your deductible, insurance isn’t really helping. You’ll pay most or even all of the repair out of pocket, and the claim still goes on your record.

That’s the part many homeowners overlook.

Even small claims can affect future premiums, eligibility, or renewal decisions. Insurance is designed for meaningful losses, not routine repairs.

This is why many experienced homeowners quietly handle smaller issues themselves, especially when costs fall within a few thousand dollars of the deductible.

It’s not about hiding damage. It’s about using insurance strategically.

Filing a claim should create a clear financial benefit, not just emotional relief. When insurance pays a significant portion of the repair, the claim usually makes sense. When it doesn’t, the long-term cost can outweigh the short-term help.

Understanding this changes how you view insurance.

Instead of treating it as a reflex or something you automatically use, begin treating it as a tool. And tools work best when you know exactly when to use them and when not to.

4 Real-World Deductible Examples

Abstract explanations only go so far. Deductibles make the most sense when you see how they play out in real situations.

Example one: minor water damage.

A supply line fails and damages part of a kitchen. Repairs total $3,200. The homeowner has a $2,500 deductible. Insurance approves the claim but only pays $700. The homeowner covers most of the cost, and the claim still appears on their record.

Financially, that claim provided very little benefit.

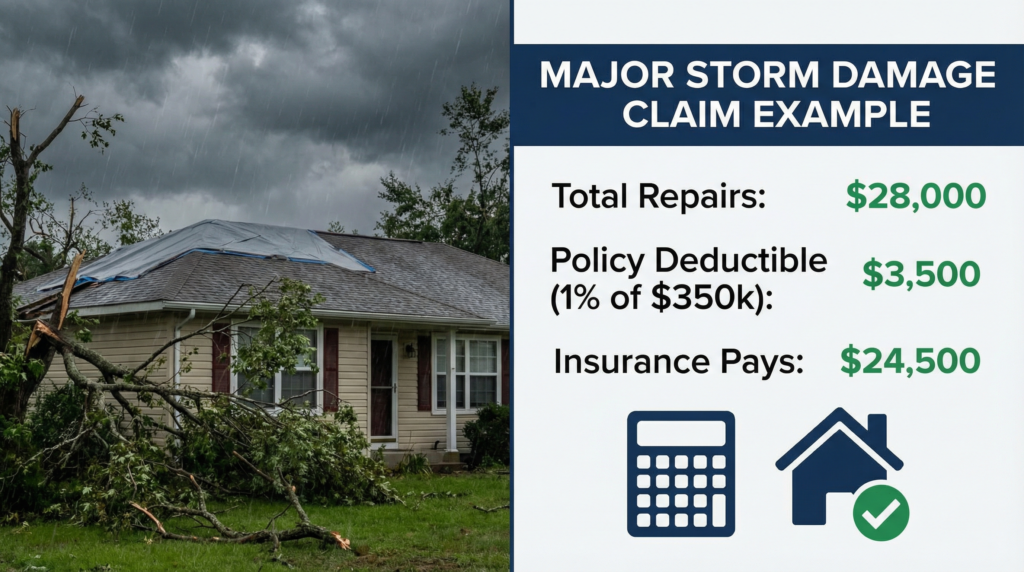

Example two: major storm damage.

A windstorm damages the roof and causes interior water damage. Total repairs come to $28,000. The policy includes a 1% wind deductible on a $350,000 home, or a $3,500 deductible. Insurance pays $24,500. In this case, the deductible is significant, but insurance clearly fulfills its role.

Example three: deductible surprise.

A homeowner believes they have a $1,000 deductible. After a hailstorm, they discover their policy uses a separate 2% deductible for wind and hail. On a $400,000 home, that’s $8,000 out of pocket before insurance contributes anything.

The claim is approved but the cost feels shocking because the deductible wasn’t fully understood beforehand.

Example four: choosing not to file.

A homeowner experiences $2,800 in damage with a $2,500 deductible. Instead of filing, they pay for repairs themselves and avoid a claim on their record.

Sometimes, the smartest insurance decision is not using insurance at all.

These examples highlight the same lesson: deductibles don’t just affect claims, they shape outcomes. When you understand them in advance, there are fewer surprises when it matters most.

Deductibles, Claims History, and Long-Term Cost

Deductibles don’t exist in isolation. They interact directly with your claims history. Every time you file a claim, and even a small one, it becomes part of your insurance record. And while a single claim doesn’t automatically cause a premium increase, patterns matter.

Multiple claims within a short period can lead to:

- Higher renewal premiums

- Reduced policy options

- Non-renewal in some cases

This is why deductibles quietly influence behavior.

A higher deductible naturally discourages small claims. Fewer small claims mean a cleaner claims history, which often leads to better pricing and more flexibility over time.

On the flip side, a very low deductible makes filing feel painless in the moment, but it can increase long-term costs if it leads to frequent claims that insurance was never meant to absorb.

Insurers price policies based on probability. A homeowner who files multiple small claims is statistically more likely to file again. Deductibles help insurers filter that risk.

This doesn’t mean you should avoid filing valid claims. It means you should be intentional.

The deductible isn’t just about what you pay today. It’s about how often you engage the insurance system and how that history follows you long after the repair is finished.

Do Deductibles Reset Every Year?

Another common point of confusion is whether deductibles actually reset each year.

In most home insurance policies, deductibles do not accumulate or carry over like a health insurance deductible. They apply per claim, not per year.

That means if you file two separate claims in the same year, you typically pay the deductible twice… once for each claim. However, there’s an important nuance. If multiple damages come from the same event, they’re usually grouped under one claim and one deductible. A single storm that damages the roof and causes interior water damage is often treated as one loss.

But separate events, even close together, usually mean separate deductibles.

This is why timing and cause matter so much.

Homeowners sometimes assume that once they’ve paid their deductible, insurance will fully cover additional losses that year. That’s rarely how it works.

Each claim stands on its own. Understanding this prevents surprises and helps homeowners plan realistically, especially in years where multiple incidents occur.

Deductibles aren’t annual thresholds. They’re event-based filters. And knowing that difference helps you decide when filing a claim truly makes sense, and when it doesn’t.

Final Conclusion

By now, deductibles should feel a lot less abstract.

They aren’t just a number buried in your policy. They’re a decision tool and one that shapes how you use insurance, how much you pay over time, and how often you interact with the claims process.

When you understand how deductibles work, insurance stops feeling reactive. You stop filing claims out of frustration or panic, and start making deliberate choices based on cost, risk, and long-term impact.

A higher deductible doesn’t mean worse coverage. A lower deductible doesn’t always mean better outcomes. The right deductible is the one that matches your financial reality, not just your desire for low monthly premiums or quick relief after a loss.

If there’s one takeaway here then it’s this:

Insurance works best when it’s used for meaningful events and not routine repairs, and deductibles are the filter that enforces that design.

Thanks for reading here.

Leave a Reply