“I Thought Insurance Covered Big Problems.” Most people don’t buy home insurance because they love paperwork. They buy it because it feels like protection.

A quiet agreement with the universe that says: If something big goes wrong, I won’t be ruined.

That belief is almost universal. Fire? Covered. Storm damage? Covered. Flooded basement? Surely covered. The logic feels obvious – insurance exists for expensive, stressful disasters. You know, the things you can’t handle on your own. And for years, that belief goes completely unchallenged.

You pay the premium. You never file a claim. Nothing bad happens. Every uneventful year reinforces the idea that your house is handled and that the policy is a safety net just sitting there and waiting.

But insurance doesn’t work on intuition.

- It doesn’t care how big the damage feels.

- It doesn’t care how sudden the stress is.

- It doesn’t even care whether the situation seems fair.

Insurance works on definitions.

It works on categories, on exclusions, and on language written by lawyers, not homeowners.

And the moment something finally does go wrong, the moment you actually need that safety net – that’s when most people discover the uncomfortable truth…

Home insurance does not cover “big problems”. It only covers very specific ones.

Water Damage Is Not One Thing

Ask any homeowner what water damage is, and you’ll get a simple answer…

Water went where it wasn’t supposed to.

But insurance doesn’t see water as one thing. It sees types of water. And those types matter more than the damage itself.

To a policy, water from a burst pipe is not the same as water from the ground. Rain entering through a sudden roof opening is not the same as water slowly seeping through a foundation wall. A broken appliance is different from rising groundwater, even if the result looks identical.

Two basements can be flooded to the same depth, with the same ruined flooring and the same soaked drywall, and only one of them may be covered.

That’s because insurance focuses on how the water entered, not what it destroyed.

- Was it sudden and accidental?

- Was it internal or external?

- Was it preventable through maintenance?

These questions decide everything.

This is where most homeowners start to feel confused. They’re staring at visible damage, but the insurer is investigating invisible causes. And if the cause falls into the wrong category and even slightly, then the claim can fail utterly.

To insurance, water damage isn’t about the mess. It’s about the story behind the mess.

The Leak That Took Years And Not Minutes

One of the fastest ways a claim gets denied is a single word buried deep in your policy:

Gradual.

Insurance loves sudden events. It hates slow ones.

A pipe that bursts overnight? Possibly covered.

A pipe that dripped for months behind a wall? Almost never.

From the insurer’s perspective, gradual damage isn’t an accident but it’s maintenance. And maintenance is considered the homeowner’s responsibility, even if the homeowner had no idea the problem existed.

That’s the painful part.

- You don’t need to be negligent.

- You don’t need to ignore warning signs.

- You just need time to pass.

A slow leak, hidden behind drywall or under flooring, can quietly cause thousands in damage. But when an adjuster sees water stains, corrosion, or mold growth patterns that suggest long-term exposure, the conclusion is often immediate…

This didn’t happen suddenly. Therefore, it isn’t covered.

To the homeowner, the damage feels sudden because the discovery was sudden. But insurance doesn’t care when you noticed the problem, only when it likely began.

And in that gap between discovery and origin, coverage often disappears.

Flooding Isn’t What You Think

Ask someone if their home insurance covers floods, and many will say yes confidently.

They’re usually wrong.

In everyday language, a flood is any situation where water overwhelms your home. Heavy rain, backed-up drains, water rushing in from outside – it all feels like flooding.

But insurance uses a much narrower definition.

If water rises from the ground up, even by an inch, it is typically classified as a flood. And most standard home insurance policies specifically exclude flood damage.

- It doesn’t matter if the water came from relentless rain.

- It doesn’t matter if your neighborhood has never flooded before.

- It doesn’t matter if the storm was historic.

If the water originated outside the home and entered by rising, spreading, or pooling on the ground, the claim is often denied unless you carry a separate flood policy.

This is one of the most expensive misunderstandings in home ownership.

- People assume storms equal coverage.

- They assume nature counts as an accident.

- They assume devastation automatically triggers help.

But to insurance, flooding is a separate risk and one you must actively opt into. And by the time most people learn that distinction, they’re already standing in water with no coverage behind them.

Earth Moves And Insurance Walks Away

There’s a quiet assumption most homeowners make without ever saying it out loud.

“The ground beneath my house is solid.”

And most of the time, that assumption holds, until it doesn’t. Cracks appear in walls. Doors stop closing. Floors begin to slope. Sometimes it’s subtle. Sometimes it’s dramatic. Either way, the damage feels serious and structural and is exactly the kind of thing insurance should help with.

But this is where another major exclusion shows up.

Earth movement.

Insurance policies usually group earthquakes, sinkholes, landslides, soil shifting, and settling into one category, and then exclude the entire category outright.

It doesn’t matter if the movement was slow or sudden.

It doesn’t matter if it followed heavy rain or drought.

It doesn’t matter if you live nowhere near a fault line.

If the ground moved and your home reacted, the insurer’s position is often the same… “This is not a covered peril.”

From their perspective, the earth is unstable by nature. And anything tied to that instability is considered not insurable under a standard policy.

So when a foundation cracks or a slab shifts, homeowners are often left stunned, facing one of the most expensive repairs imaginable, with zero help from the policy they thought existed for moments like this.

Mold Is The Silent Claim Killer Itself

Few words cause faster panic in a homeowner than the word mold.

It spreads quietly. It looks dangerous. It’s expensive to remove properly.

So when mold appears, many people assume insurance will step in, especially if water damage was involved. But mold sits in one of the most restricted areas of home insurance.

In many policies, mold is either completely excluded or capped at a very low amount, sometimes just a few thousand dollars, regardless of how extensive the damage becomes.

Why? Insurers don’t view mold as a primary event. They see it as a result, as something that grows because water wasn’t addressed quickly enough, or because moisture existed over time.

Even if the original water damage was covered, the mold that follows may not be. And if the mold is linked to a slow leak, humidity issue, or ventilation problem? The denial becomes almost automatic.

This creates a brutal situation and one where the water claim might be partially approved, while the mold remediation that is often the most expensive part, is fully rejected.

To homeowners, mold feels like the disaster. To insurance, it’s often treated like a preventable consequence.

What Happens When You Leave the House

Most people think coverage follows ownership. If you own the home, it’s insured.

But insurance doesn’t just care who owns the house; it cares whether the house is being lived in. Many policies include vacancy or non-occupancy clauses that quietly change coverage when a home sits empty for too long. And the clock starts ticking faster than most people realize.

- A long vacation.

- A temporary move.

- A home waiting to be sold or renovated.

After a certain period – sometimes as short as 30 or 60 days, coverage can be reduced or suspended entirely for specific risks, especially water damage and vandalism.

The logic from the insurer’s side is simple… empty homes deteriorate faster and suffer more severe damage before anyone notices.

But homeowners rarely think to notify their insurer when they leave for extended periods. They assume silence keeps things the same. Then something happens while the house is empty, like a pipe freezes, or perhaps a leak spreads, or even a break-in occurs.

And that’s when they discover the truth.

The house was insured. But not in the way they thought.

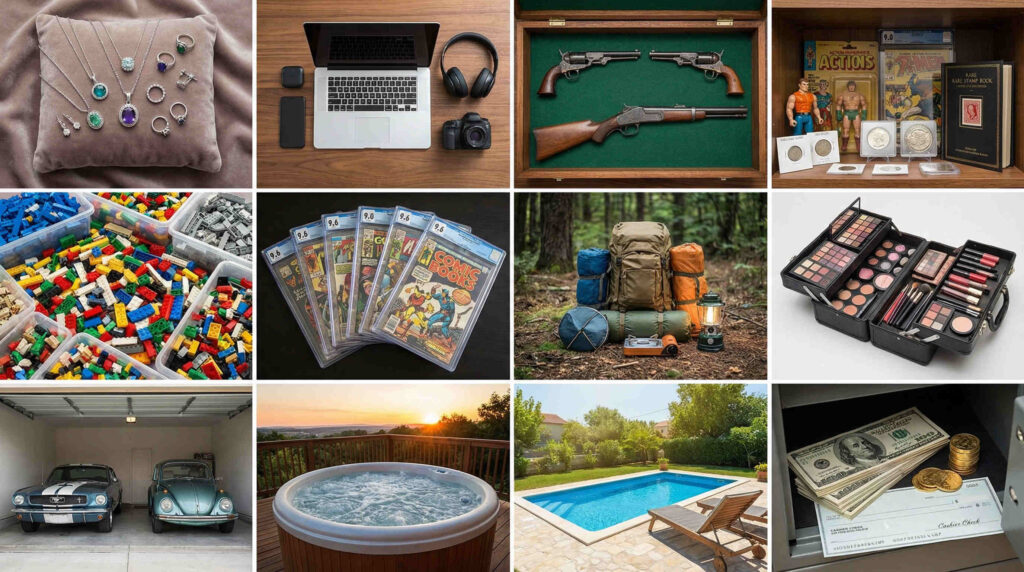

Your Belongings Aren’t Worth What You Think

When people imagine an insurance claim, they usually picture walls, floors, and roofs. But some of the biggest disappointments happen with the things inside the house.

Personal property feels straightforward: if you own it and it’s damaged, insurance replaces it. But that assumption runs straight into a maze of limits most people never see coming.

Many policies place sub-limits on specific categories of items, regardless of how valuable they actually are. These can include the following.

- Jewelry.

- Electronics.

- Firearms.

- Collectibles.

- Cash equivalents.

You might own a $6,000 ring, but the policy might cap jewelry coverage at $1,500 unless you added a rider. You might lose thousands in electronics to a surge or leak, only to find depreciation slashes the payout in half.

And that’s another surprise: actual cash value.

Instead of replacing items at today’s prices, some policies deduct for age and wear. A five-year-old TV isn’t replaced as much as it’s valued. And that value can be painfully low.

To the homeowner, loss feels absolute. To insurance, it’s calculated.

Unless you’ve reviewed limits, added endorsements, and documented belongings in advance, personal property coverage often feels generous right up until the moment you need it.

The Denial Letter Moment

This is the moment almost no one is prepared for.

The damage has already happened. The stress is already real. And the claim has been filed with confidence.

An adjuster visits. Photos are taken. Notes are made. There’s a strange sense of relief like help is finally on the way. Then the letter arrives.

- It doesn’t sound cruel.

It doesn’t sound emotional.

It sounds professional. - “After reviewing your policy…”

“Based on the findings…”

“Unfortunately, this loss is excluded…”

This is where homeowners feel blindsided.

They remember paying premiums. They remember being told they were covered. They remember doing everything right, or at least nothing wrong. But the denial letter doesn’t argue with feelings. It points to paragraphs and clauses and definitions buried deep in the policy.

And suddenly, the most expensive lesson of home ownership becomes clear.

Insurance doesn’t deny claims because it wants to.

It denies claims because the contract allows it to.

By the time this realization sets in, the damage is already yours to handle… financially, emotionally, and completely.

Know your insurance and its terms.

Insurance Isn’t Protection; Insurance Is A Contract

This is the shift most homeowners never make until it’s too late.

Insurance feels like protection. But legally, it isn’t precisely that. Legally it is a contract.

It’s an actual contract that lists exactly what it will do, and far more importantly, what it won’t. It’s a contract that doesn’t care about expectations, assumptions, or fairness, but only wording.

Once you understand this, everything changes.

You stop asking, “Am I covered?”, and start asking, “Under what conditions would this be covered?”

You stop assuming disasters are included, and start identifying which risks you’re actually carrying yourself. Home insurance isn’t designed to eliminate risk. It’s designed to transfer specific risks and leave the rest with you.

The danger isn’t that insurance fails, but that people misunderstand what it was ever meant to do.

When homeowners finally see insurance for what it is – a legal agreement with sharp edges, they can make smarter choices. Add coverage where it matters. Accept gaps where it doesn’t. Avoid the shock that comes from learning all of this after a loss.

Remember that the most expensive time to read your policy is after something goes wrong.

Leave a Reply